華爾街大空頭的最新做空對(duì)象:一家金融服務(wù)巨頭

Will Daniel

2024-01-20

知名做空機(jī)構(gòu)稱,明晟公司的價(jià)值比宣傳的要低65%。

文本設(shè)置

文本設(shè)置

Plus(0條)

Plus(0條)

長(zhǎng)期以來(lái),美國(guó)的金融服務(wù)巨頭明晟公司(MSCI Inc.)一直是投資者投資組合的重要組成部分。許多全球最大的基金管理公司每天都依賴明晟公司的股票、固定收益和房地產(chǎn)指數(shù),以及其分析工具和環(huán)境、社會(huì)和公司治理(以下簡(jiǎn)稱ESG)評(píng)級(jí)來(lái)運(yùn)營(yíng)。這一有利地位使該公司成為近期的強(qiáng)勢(shì)集團(tuán),其股價(jià)在過(guò)去五年里飆升了逾225%。

但知名做空機(jī)構(gòu)Spruce Point Capital Management在1月17日發(fā)布了一份利空?qǐng)?bào)告,稱明晟公司增長(zhǎng)前景疲軟、估值難以為繼、會(huì)計(jì)和財(cái)務(wù)報(bào)告選擇存疑,可能導(dǎo)致其股價(jià)暴跌55%至65%,旨在打破明晟公司的光環(huán)。

此外,該做空機(jī)構(gòu)還聲稱,如果要對(duì)ESG評(píng)級(jí)領(lǐng)導(dǎo)者明晟公司進(jìn)行評(píng)估,其ESG評(píng)級(jí)都不到及格線,原因是其治理存在裙帶關(guān)系問(wèn)題。

Spruce Point的團(tuán)隊(duì)在1月17日的報(bào)告中寫(xiě)道:“我們認(rèn)為,明晟公司是典型案例,這家陷入困境的公司在進(jìn)行價(jià)值破壞性(甚至更糟糕的裙帶關(guān)系式)收購(gòu)和股票回購(gòu)的同時(shí),未能實(shí)現(xiàn)公司轉(zhuǎn)型,而是通過(guò)濫用財(cái)務(wù)報(bào)告和會(huì)計(jì)手段來(lái)提高收益。”

Spruce Point的創(chuàng)始人及首席投資官本·阿克斯勒在接受《財(cái)富》雜志采訪時(shí)解釋道,他在對(duì)明晟公司的調(diào)查中發(fā)現(xiàn)該公司出現(xiàn)多個(gè)“典型的危險(xiǎn)信號(hào)”,這表明,該公司股票的交易溢價(jià)不應(yīng)該接近目前的水平。從明晟公司轉(zhuǎn)而在財(cái)務(wù)報(bào)告里關(guān)注經(jīng)調(diào)整收益而非利潤(rùn)率,到斥資9.5億美元收購(gòu)商業(yè)房地產(chǎn)分析公司Real Capital Analytics,阿克斯勒認(rèn)為,有“證據(jù)表明該公司做法與股東利益不一致”,而且存在“治理問(wèn)題”,可能會(huì)給公司股票帶來(lái)隱患。

明晟公司的一位代表通過(guò)電子郵件對(duì)《財(cái)富》雜志表示,該公司“斷然反駁”Spruce Point 在1月17日?qǐng)?bào)告中的說(shuō)法。該代表說(shuō):“這份報(bào)告是一家做空機(jī)構(gòu)蓄意針對(duì)我們的利益相關(guān)者發(fā)布的具有誤導(dǎo)性的虛假信息,而且其內(nèi)容缺乏完整性,目的是轉(zhuǎn)移人們對(duì)明晟公司取得的成功和獲得機(jī)遇的注意力。我們公司擁有濃厚的合規(guī)和道德文化氛圍,我們的行為準(zhǔn)則,以及我們致力于開(kāi)展業(yè)內(nèi)領(lǐng)先的公司治理實(shí)踐奠定了相關(guān)文化基礎(chǔ),這一點(diǎn)在我們強(qiáng)有力的財(cái)務(wù)控制和透明的財(cái)務(wù)報(bào)告中均有所體現(xiàn)。”

阿克斯勒澄清道,Spruce Point“絕沒(méi)有指控明晟公司存在任何違法行為”,他認(rèn)為,即使該公司目前的估值遠(yuǎn)遠(yuǎn)偏離了基準(zhǔn),只要假以時(shí)日,明晟公司仍然有可能扭轉(zhuǎn)局面。他說(shuō):“我們希望他們能夠聽(tīng)取我們的一些批評(píng)意見(jiàn),我認(rèn)為很多問(wèn)題可以歸結(jié)為:他們能否改善治理,解決我們概述的問(wèn)題,并提高透明度?”

以下是阿克斯勒對(duì)明晟公司的主要擔(dān)憂。

高估值和客戶保留問(wèn)題

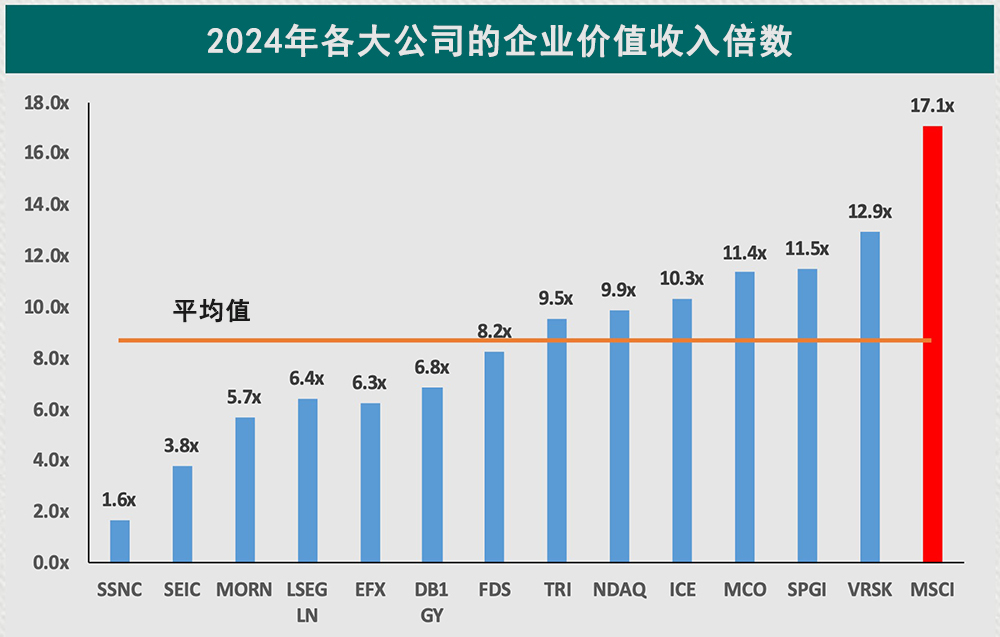

首先,阿克斯勒和Spruce Point認(rèn)為,與同行相比,明晟公司的估值過(guò)高,難以為繼。在1月16日發(fā)布利空?qǐng)?bào)告前,這家金融服務(wù)巨頭的企業(yè)價(jià)值收入倍數(shù)約為17倍(投資者用來(lái)衡量股票相對(duì)價(jià)值的常用指標(biāo)),遠(yuǎn)遠(yuǎn)高于標(biāo)準(zhǔn)普爾全球(S&P Global)、納斯達(dá)克(Nasdaq)和晨星公司(Morningstar)的企業(yè)價(jià)值收入倍數(shù),分別約為11倍、10倍和6倍。

圖片來(lái)源:SPRUCE POINT CAPITAL MANAGEMENT

Spruce Point指出,除了估值過(guò)高之外,明晟公司在客戶保留方面也開(kāi)始出現(xiàn)問(wèn)題。阿克斯勒解釋道:“人們認(rèn)為,明晟公司的客戶保留率很高,而且其產(chǎn)品粘性高”,這導(dǎo)致該股的估值很高,但他認(rèn)為“這不是一成不變的”。Spruce Point稱,明晟公司核心指數(shù)業(yè)務(wù)的客戶保留率在過(guò)去四個(gè)季度有所下降,該業(yè)務(wù)占其收入的58%。除此之外,該部門(mén)約17%的收入來(lái)自貝萊德(BlackRock)。Spruce Point表示,貝萊德“采用了自我指數(shù)化”,降低了明晟公司產(chǎn)品的效用。

Spruce Point還對(duì)60家明晟公司的客戶進(jìn)行了調(diào)查,發(fā)現(xiàn)“相當(dāng)大比例”的客戶指出,在過(guò)去12個(gè)月里,明晟公司的競(jìng)爭(zhēng)對(duì)手?jǐn)U大了服務(wù)范圍。阿克斯勒和他的團(tuán)隊(duì)認(rèn)為,來(lái)自彭博社(Bloomberg)、曠勢(shì)[Qontigo,德意志證券交易所(Deutsche B?rse)旗下公司]和其他公司的競(jìng)爭(zhēng)日趨激烈,已經(jīng)開(kāi)始影響明晟公司的客戶保留率。

阿克斯勒告訴《財(cái)富》雜志,還有跡象表明,明晟公司正在對(duì)現(xiàn)有客戶采取“懲罰性提價(jià)”手段,以維持收入增長(zhǎng)。如果沒(méi)有采取這些提價(jià)措施,Spruce Point預(yù)計(jì)其2023年新增經(jīng)常性銷售額就將下降40%。

收購(gòu)存疑和裙帶關(guān)系

阿克斯勒和他的團(tuán)隊(duì)認(rèn)為,除了客戶保留率下降和競(jìng)爭(zhēng)加劇之外,明晟公司為了在短期內(nèi)提高收益,選擇進(jìn)行的部分收購(gòu)并不合理。

他們指出,明晟公司2021年以9.5億美元收購(gòu)商業(yè)地產(chǎn)數(shù)據(jù)和分析供應(yīng)商Real Capital Analytics可能并不符合股東的最佳利益。明晟公司收購(gòu)Real Capital Analytics的價(jià)格約為其運(yùn)營(yíng)收入的13倍,息稅折舊攤銷前利潤(rùn)(EBITDA)的48倍,估值過(guò)高。Spruce Point的簡(jiǎn)短報(bào)告稱:“我們認(rèn)為,此次收購(gòu)充滿挑戰(zhàn),表明明晟公司傾向于通過(guò)激進(jìn)的收入和成本核算手段來(lái)夸大其財(cái)務(wù)業(yè)績(jī)。”

報(bào)道隨后引用了一位“知情前高管”的話,稱此次收購(gòu)讓該公司陷入“徹底失控的糟糕局勢(shì)”,并聲稱明晟公司沒(méi)有進(jìn)行“詳盡的盡職調(diào)查”。

根據(jù)Spruce Point的說(shuō)法,除了收購(gòu)Real Capital Analytics之外,管理層的多項(xiàng)收購(gòu)和行動(dòng)都有裙帶關(guān)系的跡象。

這家做空機(jī)構(gòu)指出,明晟公司最初被稱為摩根士丹利資本國(guó)際公司(Morgan Stanley Capital International),該公司與同名投行關(guān)系密切。報(bào)告寫(xiě)道:“太讓人意外了!我們發(fā)現(xiàn)明晟公司最近采取了一種可疑的收購(gòu)和結(jié)盟模式,從而使摩根士丹利(Morgan Stanley)和明晟公司的高管受益。我們稱之為裙帶關(guān)系式交易,最近出現(xiàn)很多這樣的例子。”

Spruce Point舉了三個(gè)具體例子來(lái)佐證其說(shuō)法。首先,明晟公司于2022年與數(shù)字資產(chǎn)金融服務(wù)公司Menai Financial Group達(dá)成協(xié)議,以未披露的條款為其提供建議。但Menai是由摩根士丹利的前聯(lián)席總裁佐伊·克魯茲創(chuàng)立的。同樣,在2023年,明晟公司以10倍于銷售額的價(jià)格收購(gòu)了專注于私募市場(chǎng)的數(shù)據(jù)和分析公司Burgiss,而明晟公司前執(zhí)行委員會(huì)成員杰伊·麥克納馬拉曾經(jīng)擔(dān)任Burgiss的總裁。最后,在2023年12月,明晟公司以一筆未披露的金額收購(gòu)了財(cái)富技術(shù)平臺(tái)Fabric,后者的聯(lián)合創(chuàng)始人曾經(jīng)是摩根士丹利的首席風(fēng)險(xiǎn)官。

同樣,阿克斯勒和Spruce Point并未在此指控該公司存在任何違法行為,但他們對(duì)明晟公司管理層的這些收購(gòu)決策提出了質(zhì)疑。

“問(wèn)題是:他們完成這些交易,是因?yàn)檫@些交易符合明晟公司作為一家企業(yè)的最佳利益,還是因?yàn)檫@些交易讓摩根士丹利和明晟公司的內(nèi)部人士受益?”阿克斯勒對(duì)《財(cái)富》雜志表示。“我們?cè)噲D通過(guò)這份報(bào)告指出,我們最近發(fā)現(xiàn)了一種可疑的模式,即這些交易和聯(lián)盟最終涉及摩根士丹利和明晟公司的內(nèi)部人士。”

會(huì)計(jì)方面的擔(dān)憂,以及一家ESG評(píng)級(jí)為“F”的相關(guān)領(lǐng)域領(lǐng)導(dǎo)者

Spruce Point提出的另一個(gè)關(guān)切涉及會(huì)計(jì)和報(bào)告問(wèn)題。首先,這家做空機(jī)構(gòu)指出,明晟公司已經(jīng)停止提供利潤(rùn)率指引,而是“修改了有關(guān)其具有吸引力的現(xiàn)金生成情況的措辭,同時(shí)強(qiáng)調(diào)經(jīng)調(diào)整每股收益”。

該做空機(jī)構(gòu)的報(bào)告稱,明晟公司還“希望投資者忽略與軟件開(kāi)發(fā)活動(dòng)相關(guān)的實(shí)際現(xiàn)金成本”,估計(jì)該公司真實(shí)的經(jīng)調(diào)整每股收益比2021年報(bào)告的低28%,比2022年報(bào)告的低13%。

從“忽略”重組成本,到誤把本應(yīng)計(jì)入成本的收購(gòu)成本計(jì)入資本,Spruce Point詳細(xì)列舉了一系列會(huì)計(jì)問(wèn)題,稱明晟公司應(yīng)該解決這些股東關(guān)切的問(wèn)題。

最后,Spruce Point表示,明晟公司的ESG業(yè)務(wù)正在面臨日益激烈的競(jìng)爭(zhēng)。自2020年以來(lái),ESG評(píng)級(jí)業(yè)務(wù)一直是明晟公司的亮點(diǎn),運(yùn)營(yíng)收入從1.38億美元上升至2.97億美元。但Spruce Point認(rèn)為,“增長(zhǎng)的井噴期的終結(jié),不僅來(lái)自于ESG的阻力、監(jiān)管的不確定性以及ESG的市場(chǎng)表現(xiàn)不佳,還[由于]明晟公司特有的問(wèn)題導(dǎo)致客戶流失。”

阿克斯勒告訴《財(cái)富》雜志:“我們認(rèn)為,他們?cè)谶@一領(lǐng)域的競(jìng)爭(zhēng)優(yōu)勢(shì)正在縮小。彭博社正在強(qiáng)化解決方案。穆迪(Moody’s)、納斯達(dá)克等一些交易所也能夠收集ESG數(shù)據(jù)……因此,我們認(rèn)為,這項(xiàng)業(yè)務(wù)正在放緩,企業(yè)價(jià)值收入倍數(shù)應(yīng)該會(huì)被壓縮。”

除此之外,如果你用環(huán)境、社會(huì)和公司治理的標(biāo)準(zhǔn)對(duì)明晟公司進(jìn)行評(píng)級(jí),它的表現(xiàn)就可能有負(fù)眾望。作為一家金融服務(wù)公司,環(huán)境、社會(huì)和公司治理標(biāo)準(zhǔn)中的環(huán)境部分對(duì)明晟公司來(lái)說(shuō)并不是什么大問(wèn)題。但阿克斯勒認(rèn)為,該公司的治理問(wèn)題非常嚴(yán)重,總體ESG評(píng)級(jí)可能會(huì)獲得“F”評(píng)級(jí)。

據(jù)Spruce Point稱,明晟公司存在的問(wèn)題不勝枚舉。例如,明晟公司的首席會(huì)計(jì)官于2023年8月辭職,但無(wú)人接替。明晟公司的一名董事還與軟件公司SolarWinds有牽連,該公司在2023年10月底被美國(guó)證券交易委員會(huì)(SEC)指控欺詐。此外,明晟公司的審計(jì)師嚴(yán)重缺乏美國(guó)會(huì)計(jì)經(jīng)驗(yàn)。阿克斯勒還指出,明晟公司推出的指數(shù)可能會(huì)使該公司的“社會(huì)”評(píng)級(jí)受到質(zhì)疑,其中包括一些關(guān)注中國(guó)或航空航天和國(guó)防股票的指數(shù)。

阿克斯勒說(shuō):“明晟公司是ESG評(píng)級(jí)的領(lǐng)導(dǎo)者,但沒(méi)有人真正對(duì)該公司進(jìn)行評(píng)級(jí)。我認(rèn)為我們正在試圖堅(jiān)持獨(dú)立的觀點(diǎn)。當(dāng)我們做空這只股票時(shí),不一定是毫無(wú)偏見(jiàn)的,但我認(rèn)為,我們?cè)噲D質(zhì)疑的是,一家對(duì)其他公司的ESG要素進(jìn)行評(píng)級(jí)的公司是否經(jīng)得起評(píng)估檢驗(yàn)?我們發(fā)現(xiàn)該公司存在很多不足之處,很多地方亟需改進(jìn)。”(財(cái)富中文網(wǎng))

譯者:中慧言-王芳

長(zhǎng)期以來(lái),美國(guó)的金融服務(wù)巨頭明晟公司(MSCI Inc.)一直是投資者投資組合的重要組成部分。許多全球最大的基金管理公司每天都依賴明晟公司的股票、固定收益和房地產(chǎn)指數(shù),以及其分析工具和環(huán)境、社會(huì)和公司治理(以下簡(jiǎn)稱ESG)評(píng)級(jí)來(lái)運(yùn)營(yíng)。這一有利地位使該公司成為近期的強(qiáng)勢(shì)集團(tuán),其股價(jià)在過(guò)去五年里飆升了逾225%。

但知名做空機(jī)構(gòu)Spruce Point Capital Management在1月17日發(fā)布了一份利空?qǐng)?bào)告,稱明晟公司增長(zhǎng)前景疲軟、估值難以為繼、會(huì)計(jì)和財(cái)務(wù)報(bào)告選擇存疑,可能導(dǎo)致其股價(jià)暴跌55%至65%,旨在打破明晟公司的光環(huán)。

此外,該做空機(jī)構(gòu)還聲稱,如果要對(duì)ESG評(píng)級(jí)領(lǐng)導(dǎo)者明晟公司進(jìn)行評(píng)估,其ESG評(píng)級(jí)都不到及格線,原因是其治理存在裙帶關(guān)系問(wèn)題。

Spruce Point的團(tuán)隊(duì)在1月17日的報(bào)告中寫(xiě)道:“我們認(rèn)為,明晟公司是典型案例,這家陷入困境的公司在進(jìn)行價(jià)值破壞性(甚至更糟糕的裙帶關(guān)系式)收購(gòu)和股票回購(gòu)的同時(shí),未能實(shí)現(xiàn)公司轉(zhuǎn)型,而是通過(guò)濫用財(cái)務(wù)報(bào)告和會(huì)計(jì)手段來(lái)提高收益。”

Spruce Point的創(chuàng)始人及首席投資官本·阿克斯勒在接受《財(cái)富》雜志采訪時(shí)解釋道,他在對(duì)明晟公司的調(diào)查中發(fā)現(xiàn)該公司出現(xiàn)多個(gè)“典型的危險(xiǎn)信號(hào)”,這表明,該公司股票的交易溢價(jià)不應(yīng)該接近目前的水平。從明晟公司轉(zhuǎn)而在財(cái)務(wù)報(bào)告里關(guān)注經(jīng)調(diào)整收益而非利潤(rùn)率,到斥資9.5億美元收購(gòu)商業(yè)房地產(chǎn)分析公司Real Capital Analytics,阿克斯勒認(rèn)為,有“證據(jù)表明該公司做法與股東利益不一致”,而且存在“治理問(wèn)題”,可能會(huì)給公司股票帶來(lái)隱患。

明晟公司的一位代表通過(guò)電子郵件對(duì)《財(cái)富》雜志表示,該公司“斷然反駁”Spruce Point 在1月17日?qǐng)?bào)告中的說(shuō)法。該代表說(shuō):“這份報(bào)告是一家做空機(jī)構(gòu)蓄意針對(duì)我們的利益相關(guān)者發(fā)布的具有誤導(dǎo)性的虛假信息,而且其內(nèi)容缺乏完整性,目的是轉(zhuǎn)移人們對(duì)明晟公司取得的成功和獲得機(jī)遇的注意力。我們公司擁有濃厚的合規(guī)和道德文化氛圍,我們的行為準(zhǔn)則,以及我們致力于開(kāi)展業(yè)內(nèi)領(lǐng)先的公司治理實(shí)踐奠定了相關(guān)文化基礎(chǔ),這一點(diǎn)在我們強(qiáng)有力的財(cái)務(wù)控制和透明的財(cái)務(wù)報(bào)告中均有所體現(xiàn)。”

阿克斯勒澄清道,Spruce Point“絕沒(méi)有指控明晟公司存在任何違法行為”,他認(rèn)為,即使該公司目前的估值遠(yuǎn)遠(yuǎn)偏離了基準(zhǔn),只要假以時(shí)日,明晟公司仍然有可能扭轉(zhuǎn)局面。他說(shuō):“我們希望他們能夠聽(tīng)取我們的一些批評(píng)意見(jiàn),我認(rèn)為很多問(wèn)題可以歸結(jié)為:他們能否改善治理,解決我們概述的問(wèn)題,并提高透明度?”

以下是阿克斯勒對(duì)明晟公司的主要擔(dān)憂。

高估值和客戶保留問(wèn)題

首先,阿克斯勒和Spruce Point認(rèn)為,與同行相比,明晟公司的估值過(guò)高,難以為繼。在1月16日發(fā)布利空?qǐng)?bào)告前,這家金融服務(wù)巨頭的企業(yè)價(jià)值收入倍數(shù)約為17倍(投資者用來(lái)衡量股票相對(duì)價(jià)值的常用指標(biāo)),遠(yuǎn)遠(yuǎn)高于標(biāo)準(zhǔn)普爾全球(S&P Global)、納斯達(dá)克(Nasdaq)和晨星公司(Morningstar)的企業(yè)價(jià)值收入倍數(shù),分別約為11倍、10倍和6倍。

公司簡(jiǎn)稱注釋:SS&C科技控股公司(SSNC);SEI投資公司(SEIC);晨星公司(MORN);倫敦證券交易所集團(tuán)公司(LSEG LN);艾可菲(EFX);德意志交易所集團(tuán)(DB1 GY);慧甚研究系統(tǒng)公司(FDS);湯森路透(TRI);納斯達(dá)克(NDAQ);洲際交易所(ICE);穆迪(MCO);標(biāo)普全球(SPGI);威瑞斯克分析(VRSK);明晟公司(MSCI)

Spruce Point指出,除了估值過(guò)高之外,明晟公司在客戶保留方面也開(kāi)始出現(xiàn)問(wèn)題。阿克斯勒解釋道:“人們認(rèn)為,明晟公司的客戶保留率很高,而且其產(chǎn)品粘性高”,這導(dǎo)致該股的估值很高,但他認(rèn)為“這不是一成不變的”。Spruce Point稱,明晟公司核心指數(shù)業(yè)務(wù)的客戶保留率在過(guò)去四個(gè)季度有所下降,該業(yè)務(wù)占其收入的58%。除此之外,該部門(mén)約17%的收入來(lái)自貝萊德(BlackRock)。Spruce Point表示,貝萊德“采用了自我指數(shù)化”,降低了明晟公司產(chǎn)品的效用。

Spruce Point還對(duì)60家明晟公司的客戶進(jìn)行了調(diào)查,發(fā)現(xiàn)“相當(dāng)大比例”的客戶指出,在過(guò)去12個(gè)月里,明晟公司的競(jìng)爭(zhēng)對(duì)手?jǐn)U大了服務(wù)范圍。阿克斯勒和他的團(tuán)隊(duì)認(rèn)為,來(lái)自彭博社(Bloomberg)、曠勢(shì)[Qontigo,德意志證券交易所(Deutsche B?rse)旗下公司]和其他公司的競(jìng)爭(zhēng)日趨激烈,已經(jīng)開(kāi)始影響明晟公司的客戶保留率。

阿克斯勒告訴《財(cái)富》雜志,還有跡象表明,明晟公司正在對(duì)現(xiàn)有客戶采取“懲罰性提價(jià)”手段,以維持收入增長(zhǎng)。如果沒(méi)有采取這些提價(jià)措施,Spruce Point預(yù)計(jì)其2023年新增經(jīng)常性銷售額就將下降40%。

收購(gòu)存疑和裙帶關(guān)系

阿克斯勒和他的團(tuán)隊(duì)認(rèn)為,除了客戶保留率下降和競(jìng)爭(zhēng)加劇之外,明晟公司為了在短期內(nèi)提高收益,選擇進(jìn)行的部分收購(gòu)并不合理。

他們指出,明晟公司2021年以9.5億美元收購(gòu)商業(yè)地產(chǎn)數(shù)據(jù)和分析供應(yīng)商Real Capital Analytics可能并不符合股東的最佳利益。明晟公司收購(gòu)Real Capital Analytics的價(jià)格約為其運(yùn)營(yíng)收入的13倍,息稅折舊攤銷前利潤(rùn)(EBITDA)的48倍,估值過(guò)高。Spruce Point的簡(jiǎn)短報(bào)告稱:“我們認(rèn)為,此次收購(gòu)充滿挑戰(zhàn),表明明晟公司傾向于通過(guò)激進(jìn)的收入和成本核算手段來(lái)夸大其財(cái)務(wù)業(yè)績(jī)。”

報(bào)道隨后引用了一位“知情前高管”的話,稱此次收購(gòu)讓該公司陷入“徹底失控的糟糕局勢(shì)”,并聲稱明晟公司沒(méi)有進(jìn)行“詳盡的盡職調(diào)查”。

根據(jù)Spruce Point的說(shuō)法,除了收購(gòu)Real Capital Analytics之外,管理層的多項(xiàng)收購(gòu)和行動(dòng)都有裙帶關(guān)系的跡象。

這家做空機(jī)構(gòu)指出,明晟公司最初被稱為摩根士丹利資本國(guó)際公司(Morgan Stanley Capital International),該公司與同名投行關(guān)系密切。報(bào)告寫(xiě)道:“太讓人意外了!我們發(fā)現(xiàn)明晟公司最近采取了一種可疑的收購(gòu)和結(jié)盟模式,從而使摩根士丹利(Morgan Stanley)和明晟公司的高管受益。我們稱之為裙帶關(guān)系式交易,最近出現(xiàn)很多這樣的例子。”

Spruce Point舉了三個(gè)具體例子來(lái)佐證其說(shuō)法。首先,明晟公司于2022年與數(shù)字資產(chǎn)金融服務(wù)公司Menai Financial Group達(dá)成協(xié)議,以未披露的條款為其提供建議。但Menai是由摩根士丹利的前聯(lián)席總裁佐伊·克魯茲創(chuàng)立的。同樣,在2023年,明晟公司以10倍于銷售額的價(jià)格收購(gòu)了專注于私募市場(chǎng)的數(shù)據(jù)和分析公司Burgiss,而明晟公司前執(zhí)行委員會(huì)成員杰伊·麥克納馬拉曾經(jīng)擔(dān)任Burgiss的總裁。最后,在2023年12月,明晟公司以一筆未披露的金額收購(gòu)了財(cái)富技術(shù)平臺(tái)Fabric,后者的聯(lián)合創(chuàng)始人曾經(jīng)是摩根士丹利的首席風(fēng)險(xiǎn)官。

同樣,阿克斯勒和Spruce Point并未在此指控該公司存在任何違法行為,但他們對(duì)明晟公司管理層的這些收購(gòu)決策提出了質(zhì)疑。

“問(wèn)題是:他們完成這些交易,是因?yàn)檫@些交易符合明晟公司作為一家企業(yè)的最佳利益,還是因?yàn)檫@些交易讓摩根士丹利和明晟公司的內(nèi)部人士受益?”阿克斯勒對(duì)《財(cái)富》雜志表示。“我們?cè)噲D通過(guò)這份報(bào)告指出,我們最近發(fā)現(xiàn)了一種可疑的模式,即這些交易和聯(lián)盟最終涉及摩根士丹利和明晟公司的內(nèi)部人士。”

會(huì)計(jì)方面的擔(dān)憂,以及一家ESG評(píng)級(jí)為“F”的相關(guān)領(lǐng)域領(lǐng)導(dǎo)者

Spruce Point提出的另一個(gè)關(guān)切涉及會(huì)計(jì)和報(bào)告問(wèn)題。首先,這家做空機(jī)構(gòu)指出,明晟公司已經(jīng)停止提供利潤(rùn)率指引,而是“修改了有關(guān)其具有吸引力的現(xiàn)金生成情況的措辭,同時(shí)強(qiáng)調(diào)經(jīng)調(diào)整每股收益”。

該做空機(jī)構(gòu)的報(bào)告稱,明晟公司還“希望投資者忽略與軟件開(kāi)發(fā)活動(dòng)相關(guān)的實(shí)際現(xiàn)金成本”,估計(jì)該公司真實(shí)的經(jīng)調(diào)整每股收益比2021年報(bào)告的低28%,比2022年報(bào)告的低13%。

從“忽略”重組成本,到誤把本應(yīng)計(jì)入成本的收購(gòu)成本計(jì)入資本,Spruce Point詳細(xì)列舉了一系列會(huì)計(jì)問(wèn)題,稱明晟公司應(yīng)該解決這些股東關(guān)切的問(wèn)題。

最后,Spruce Point表示,明晟公司的ESG業(yè)務(wù)正在面臨日益激烈的競(jìng)爭(zhēng)。自2020年以來(lái),ESG評(píng)級(jí)業(yè)務(wù)一直是明晟公司的亮點(diǎn),運(yùn)營(yíng)收入從1.38億美元上升至2.97億美元。但Spruce Point認(rèn)為,“增長(zhǎng)的井噴期的終結(jié),不僅來(lái)自于ESG的阻力、監(jiān)管的不確定性以及ESG的市場(chǎng)表現(xiàn)不佳,還[由于]明晟公司特有的問(wèn)題導(dǎo)致客戶流失。”

阿克斯勒告訴《財(cái)富》雜志:“我們認(rèn)為,他們?cè)谶@一領(lǐng)域的競(jìng)爭(zhēng)優(yōu)勢(shì)正在縮小。彭博社正在強(qiáng)化解決方案。穆迪(Moody’s)、納斯達(dá)克等一些交易所也能夠收集ESG數(shù)據(jù)……因此,我們認(rèn)為,這項(xiàng)業(yè)務(wù)正在放緩,企業(yè)價(jià)值收入倍數(shù)應(yīng)該會(huì)被壓縮。”

除此之外,如果你用環(huán)境、社會(huì)和公司治理的標(biāo)準(zhǔn)對(duì)明晟公司進(jìn)行評(píng)級(jí),它的表現(xiàn)就可能有負(fù)眾望。作為一家金融服務(wù)公司,環(huán)境、社會(huì)和公司治理標(biāo)準(zhǔn)中的環(huán)境部分對(duì)明晟公司來(lái)說(shuō)并不是什么大問(wèn)題。但阿克斯勒認(rèn)為,該公司的治理問(wèn)題非常嚴(yán)重,總體ESG評(píng)級(jí)可能會(huì)獲得“F”評(píng)級(jí)。

據(jù)Spruce Point稱,明晟公司存在的問(wèn)題不勝枚舉。例如,明晟公司的首席會(huì)計(jì)官于2023年8月辭職,但無(wú)人接替。明晟公司的一名董事還與軟件公司SolarWinds有牽連,該公司在2023年10月底被美國(guó)證券交易委員會(huì)(SEC)指控欺詐。此外,明晟公司的審計(jì)師嚴(yán)重缺乏美國(guó)會(huì)計(jì)經(jīng)驗(yàn)。阿克斯勒還指出,明晟公司推出的指數(shù)可能會(huì)使該公司的“社會(huì)”評(píng)級(jí)受到質(zhì)疑,其中包括一些關(guān)注中國(guó)或航空航天和國(guó)防股票的指數(shù)。

阿克斯勒說(shuō):“明晟公司是ESG評(píng)級(jí)的領(lǐng)導(dǎo)者,但沒(méi)有人真正對(duì)該公司進(jìn)行評(píng)級(jí)。我認(rèn)為我們正在試圖堅(jiān)持獨(dú)立的觀點(diǎn)。當(dāng)我們做空這只股票時(shí),不一定是毫無(wú)偏見(jiàn)的,但我認(rèn)為,我們?cè)噲D質(zhì)疑的是,一家對(duì)其他公司的ESG要素進(jìn)行評(píng)級(jí)的公司是否經(jīng)得起評(píng)估檢驗(yàn)?我們發(fā)現(xiàn)該公司存在很多不足之處,很多地方亟需改進(jìn)。”(財(cái)富中文網(wǎng))

譯者:中慧言-王芳

The American financial services giant MSCI has long been a staple of investors’ portfolios. Many of the world’s largest money managers rely on MSCI’s equity, fixed income, and real estate indexes, as well as its analytics tools, and its ESG ratings, to operate each day. That favored position has made the company a powerhouse of late, with its stock surging more than 225% over the past five years.

But noted short-seller Spruce Point Capital Management aims to puncture MSCI’s halo, issuing a short report on January 17 that argues the company’s weak growth prospects, unsustainable valuation, and dubious accounting and financial reporting choices could lead its stock to plummet 55% to 65%.

Moreover, the short seller claimed that the ESG ratings leader MSCI would itself receive a failing ESG rating if it were to be evaluated, due to its governance issues that have an air of nepotism.

“We believe MSCI is a classic case of a struggling company failing to transform itself while engaging in value-destructive (and even worse nepotism-like) acquisitions and share repurchases with abusive financial reporting and accounting tactics to bolster earnings,” Spruce Point’s team wrote in its January 17 report.

In an interview with Fortune, Spruce Point’s founder and chief investment officer, Ben Axler, explained that he saw multiple “classic red flags” at MSCI during his investigation of the company that indicate its stock shouldn’t be trading anywhere near the premium it enjoys today. From MSCI’s shift to focusing on adjusted earnings instead of margins in its financial reporting, to its questionable $950 million acquisition of the commercial real estate analytics company Real Capital Analytics, Axler argues that there is “evidence of misalignment with shareholders” and “governance issues” that could spell trouble for stock.

An MSCI representative told Fortune via email that the company “categorically refutes the claims” made in Spruce Point’s Jan. 17 report. “This report is an intentional attempt by a short-seller to target our stakeholders with misleading, incomplete and false information that aims to distract from MSCI’s successes and opportunities,” the representative said. “MSCI has a strong culture of compliance and ethics grounded in our code of conduct and our commitment to leading corporate governance practices, demonstrated through our robust financial controls and transparent financial reporting.”

Axler clarified that Spruce Point is “definitely not alleging anything illegal,” and he thinks MSCI can still turn things around given time, even if the current valuation is way off base. “We hope they listen to some of our criticisms,” he said. “I think a lot of it boils down to: can they improve their governance, fix some of the things we’ve outlined, and be more transparent?”

Here’s a look at some of Axler’s main concerns when it comes to MSCI.

A lofty valuation and client retention issues

First and foremost, Axler and Spruce Point argue that MSCI is trading at an unsustainable and “extreme” valuation relative to its peers. The financial services giant’s enterprise value to revenue multiple, a common metric used by investors to measure the relative value of a stock, was around 17x on January 16 before the short report. That’s substantially higher than its peers S&P Global, Nasdaq, and Morningstar, at roughly 11x, 10x, and 6x, respectively.

In addition to being expensive, MSCI is beginning to have issues with customer retention, Spruce Point noted. Axler explained, “there’s a belief that [MSCI] has a high client retention rate. And it’s a sticky product,” which had led to the stock boasting a high valuation, but he believes “that’s not immutable.” The client retention rate in MSCI’s core index business, which makes up 58% of revenue, has declined for the past four quarters, Spruce Point noted. On top of that, roughly 17% of that segment’s revenue comes from BlackRock, which Spruce Point says has “embraced self-indexing,” reducing the utility of MSCI’s products.

Spruce Point also conducted a survey of 60 MSCI clients and found that “a substantial percentage” reported more outreach from competitors in the last 12 months. Axler and his team argue that rising competition from Bloomberg, Qontigo (which is owned by Deutsche B?rse), and others is beginning to impact client retention.

There are also signs that MSCI is using “punitive price increases” on existing customers to maintain revenue growth, Axler told Fortune. Without these increases, Spruce Point estimates that new recurring sales fell 40% in 2023.

Questionable acquisitions and whiffs of nepotism

Beyond waning client retention and increasing competition, Axler and his team believe that MSCI has opted for acquisitions that don’t always make sense in order to boost its earnings over the near term.

They argue that MSCI’s 2021 acquisition of the commercial real estate data and analytics provider Real Capital Analytics (RCA) for $950 million might not have been in the best interest of shareholders. MSCI purchased RCA for roughly 13 times its run-rate revenue and 48 times EBITDA, a lofty valuation. “We believe the acquisition was littered with challenges and shows MSCI’s propensity for aggressive revenue and cost accounting to inflate its financial performance,” Spruce Point’s short report reads.

The report then cites a “former executive close to the situation,” who it says called the acquisition “a dumpster fire” and claimed that MSCI did not do “enough due diligence.”

Beyond the RCA acquisition, multiple purchases and actions by management had a hint of nepotism, according to Spruce Point.

The short-seller noted that MSCI originally was called Morgan Stanley Capital International, and the company has close ties with the investment bank of the same name. “Surprise, surprise! We find that MSCI has recently engaged in a suspicious pattern of making acquisitions and alliances that benefit Morgan Stanley and MSCI alums,” the report reads. “We term this nepotism-like dealing and there are many recent examples.”

Spruce Point gave three specific examples for its claims. First, MSCI struck a deal with the digital asset financial services firm Menai Financial Group in 2022 to provide advice on undisclosed terms. But Menai was founded by Zoe Cruz, a former co-president at Morgan Stanley. Similarly, in 2023, MSCI paid 10 times sales for Burgiss, a data and analytics firm that focuses on private markets, where Jay McNamara, a former executive committee member at MSCI, was president. And finally, in December 2023, MSCI paid an undisclosed amount to acquire the wealth technology platform Fabric, whose co-founder was formerly Morgan Stanley’s chief risk officer.

Again, Axler and Spruce Point are not alleging anything illegal here, but they are calling into question MSCI’s management’s decisions when it comes to these acquisitions.

“The question has to be: Are they doing these deals because they’re in the best interest for MSCI as a business or are they doing these deals because they benefit people in the sphere of Morgan Stanley and MSCI?” Axler told Fortune. “We’re trying to point out with the report that we’ve seen a suspicious pattern recently of these deals and alliances ultimately involving people within the sphere of Morgan Stanley and MSCI.”

Accounting concerns—and an ESG ratings leader with an ‘F’ rating

Another concern Spruce Point put forward touches on accounting and reporting issues. First, the short-seller notes that MSCI has stopped providing margin guidance and instead “modified its language about its attractive cash generation profile, while now emphasizing Adjusted EPS.”

The short sellers’ report alleges that MSCI also “wants investors to ignore real cash costs associated with software development activities,” estimating that the firm’s true adjusted EPS was 28% lower than what was reported in 2021 and 13% lower than what was reported in 2022.

From “ignoring” restructuring costs to incorrectly capitalizing acquisition costs that were supposed to be expensed, Spruce Point details a string of accounting issues that, it says, should be addressed by MSCI and are a concern for shareholders.

Finally, MSCI’s ESG business is facing increasing competition, according to Spruce Point. The ESG ratings business has been a bright spot for MSCI since 2020, with run rate revenue rising from $138 million to $297 million. But Spruce Point believes that “the growth spurt is ending not only from ESG pushback, regulatory uncertainty, and ESG’s market underperformance, but also [due to] MSCI-specific issues that are resulting in client loss.”

“Their competitive advantage in the business, we think, is narrowing,” Axler told Fortune. “Because you’ve got Bloomberg beefing up solutions. You’ve got Moody’s, you’ve got some of the exchanges in there, like NASDAQ, that are able to collect ESG data…So we think that business is slowing, and the multiples should be compressing.”

On top of that, if you were to rate MSCI on an environmental, social, governance scale, it might not do very well. As a financial services company, the environmental part of the ESG scale wouldn’t be much of an issue for MSCI. But Axler argued that the company’s governance issues are so serious that it would likely receive an ‘F’ ESG rating overall.

The list of issues at MSCI, according to Spruce Point, goes on and on. MSCI’s chief accounting officer, for example, resigned in August without being replaced. A director at MSCI was also involved with the software company SolarWinds, which was charged by the SEC with fraud at the end of October. And there is a serious lack of U.S. accounting experience among MSCI’s auditors. Axler also noted that MSCI has launched indices that could put the company’s “social” rating in question, including some that focus on Chinese or aerospace and defense equities.

“MSCI is an ESG ratings leader, but nobody’s really rated them. I think we’re trying to take an independent view. It’s not necessarily an unbiased one when we’re short the stock, but I think, we’re trying to question, does the company that rates others’ ESG factors stand up after a review?” Axler said. “And we find a lot of shortcomings. We think a lot of things could be improved.”

請(qǐng)打開(kāi)財(cái)富Plus APP