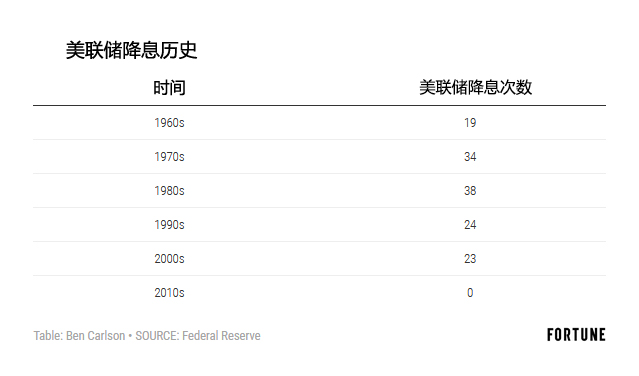

美聯(lián)儲(chǔ)降息史

|

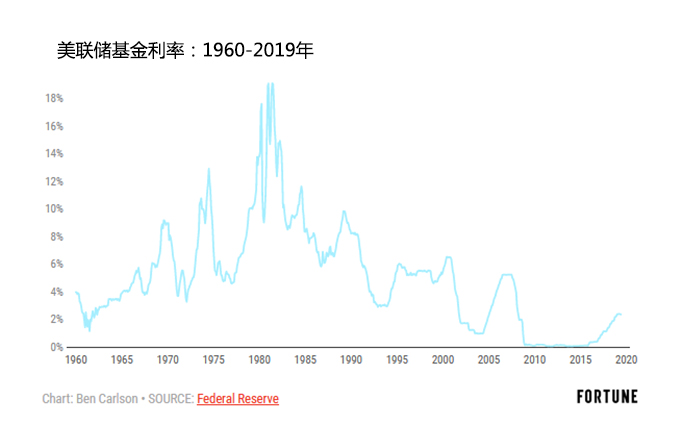

上周在眾議院金融服務(wù)委員會(huì)作證時(shí),美聯(lián)儲(chǔ)主席杰羅姆·鮑威爾暗示該機(jī)構(gòu)可能在本月底再次開會(huì)時(shí)決定下調(diào)短期利率。 歷史上下調(diào)利率并不新鮮,但美聯(lián)儲(chǔ)上次降息已經(jīng)是很久以前的事了。1960年以來,美聯(lián)儲(chǔ)將聯(lián)邦基金利率下調(diào)了近140次,每10年大概降息 23次。但2011年至今該機(jī)構(gòu)還沒有降低過利率。 |

Testifying before the House Financial Services Committee last week, Fed Chair Jerome Powell hinted that the Federal Reserve may cut short-term interest rates when they meet again later this month. A rate cut wouldn’t be anything new in terms of history but it has been a long time since the Fed last lowered their short-term interest rate. Since 1960, the Federal Reserve has cut the Fed Funds Rate nearly 140 times. That’s good enough for roughly 23 times per decade. But there hasn’t been a single rate cut this decade: |

|

顯然,這段時(shí)間一直沒有降息的最主要原因是全球金融危機(jī)過后美國(guó)利率一直處于非常低的水平。2008年12月實(shí)際利率降至零,直到2015年12月美聯(lián)儲(chǔ)終于將利率上調(diào)了0.25個(gè)百分點(diǎn),利率才開始回升。 在過去近60年時(shí)間里,美國(guó)利率平均降幅為0.5個(gè)百分點(diǎn),但和今天的市場(chǎng)或經(jīng)濟(jì)狀況類似的歷史階段并不多。目前聯(lián)邦基金利率為2.5%。2007-2009年爆發(fā)金融危機(jī)前,美聯(lián)儲(chǔ)將利率降至3%以下的次數(shù)屈指可數(shù)。 1960年以來的降息行動(dòng)中,降息前利率高于當(dāng)前利率的占92%以上,失業(yè)率高于目前水平的幾乎達(dá)到99%,還有近65%的降息出現(xiàn)在通脹率比當(dāng)前水平高的時(shí)候。 為應(yīng)對(duì)1960年至1961年初的輕微經(jīng)濟(jì)衰退,美聯(lián)儲(chǔ)主席威廉·麥克切斯尼·馬丁曾經(jīng)10次下調(diào)利率,聯(lián)邦基金利率在差不多兩年時(shí)間里一直低于3%(在此期間美聯(lián)儲(chǔ)也曾經(jīng)兩次加息)。但受衰退影響,當(dāng)時(shí)的失業(yè)率比現(xiàn)在高得多,1961年一度突破7%。 當(dāng)前美國(guó)失業(yè)率僅為3.7%,是1969年以來的最低點(diǎn)。實(shí)際上,上次美聯(lián)儲(chǔ)在失業(yè)率如此之低時(shí)下調(diào)利率就是在1969年7月,當(dāng)時(shí)的降息幅度為0.25個(gè)百分點(diǎn)。但在即將進(jìn)入70年代時(shí),通脹剛剛開始上行,所以當(dāng)時(shí)的利率遠(yuǎn)高于目前水平。1969年降息前,聯(lián)邦基金利率接近9%,而且為了抑制通脹,美聯(lián)儲(chǔ)沒過幾個(gè)月就出現(xiàn)大轉(zhuǎn)折,再次提高了利率。 1960年以來美聯(lián)儲(chǔ)在失業(yè)率和聯(lián)邦基金利率都低于4%時(shí)降息的情況只出現(xiàn)過一次,那是在1967年夏天,具體而言是當(dāng)年7月。但那次降息并未持續(xù)很長(zhǎng)時(shí)間,當(dāng)年年底前美聯(lián)儲(chǔ)就加息兩次。 進(jìn)入70年代之際,美國(guó)通脹率迅速逼近6%,而且有可能在這個(gè)10年結(jié)束時(shí)達(dá)到兩位數(shù)。現(xiàn)在美國(guó)通脹率則只有1.6%。通脹率低于2%時(shí)美聯(lián)儲(chǔ)降息的情況只在60年代初出現(xiàn)過一次,但如上文所述,當(dāng)時(shí)美國(guó)正處于衰退之中。 所以說,當(dāng)前的局勢(shì)很特殊。利率、失業(yè)率和通脹率都處于歷史上很低的水平。這可能是10多年來美聯(lián)儲(chǔ)首次降息。此外,美國(guó)股市近幾周又一次創(chuàng)下歷史新高。 2015年底美聯(lián)儲(chǔ)進(jìn)入加息周期的唯一原因很可能是讓自己隨后可以下調(diào)利率,目前該機(jī)構(gòu)的策略看來就是這樣。短期內(nèi),美聯(lián)儲(chǔ)的任何行動(dòng)都更有可能給市場(chǎng)帶來心理上的影響,而不會(huì)長(zhǎng)久地改變基本面。 市場(chǎng)受到的短期影響一直取決于投資者決定選擇怎樣的邏輯。有些人會(huì)認(rèn)為降息表明經(jīng)濟(jì)滑坡。另一些人則相信美聯(lián)儲(chǔ)降息是為了維持當(dāng)前的良好形勢(shì)。 但最終,這些短期解讀都必須得到長(zhǎng)期基本面的支持,否則就可能被視為欺騙。盡管1960年以來降息近140次,但在這期間美國(guó)股市出現(xiàn)了30次兩位數(shù)回調(diào),美國(guó)經(jīng)濟(jì)也經(jīng)歷了8次衰退。無論采取怎樣的措施,美聯(lián)儲(chǔ)都無法永遠(yuǎn)杜絕衰退或熊市。(財(cái)富中文網(wǎng)) 譯者:Charlie 審校:夏林 |

Obviously, the biggest reason there hasn’t been a rate cut this decade is that rates were on the floor for so long following the Great Financial Crisis. Rates were effectively lowered to zero in December 2008 and didn’t rise from the dead until December 2015, when the Fed finally raised rates a quarter of a percent. The average rate cut over the past 60 years or so is 50 basis points but there aren’t many historical scenarios that compare with the current market or economic situation. The Fed Funds rate currently stands at 2.5%. Before the financial crisis of 2007-2009, there have only been a handful of times where the Fed cut rates with yields below 3%. More than 92% of all rate cuts since 1960 have come from higher levels of the Fed Funds Rate. Almost 99% have come when the unemployment rate was higher than the latest reading. And nearly 65% have come when the inflation rate is higher than it currently stands. In response to a minor recession in 1960 which bled into early-1961, Fed Chair William McChesney Martin cut rates ten times while the Fed Funds Rate was below 3% over the course of two years or so (rates were also raised twice during this time). But the unemployment rate was much higher in those days because of the recession, topping out at more than 7% in 1961. The current unemployment rate stands at just 3.7%, the lowest it’s been since 1969. In fact, the last time the Fed cut interest rates with the unemployment rate so low was in July of 1969, when they cut a quarter of a percent. But yields were much higher at that time as inflation was just beginning to take off heading into the 1970s. The Federal Funds Rate was nearly 9% during that rate cut in 1969 and the Fed would actually reverse course and raise rates the very next month in an effort to stave off inflation. There was only one instance since 1960 where both the unemployment rate and the Fed Funds Rate were sub-4% when the Fed cut rates, which occurred in the summer of July 1967. That cut didn't last for long as the Fed raised rates twice before the end of that year. Inflation was fast approaching 6% heading into the 1970s and would reach double-digits by the end of that decade. The latest reading stood at just 1.6%. The only other time we’ve seen the Fed cut rates with inflation below 2% was during the early-1960s, but again that was in the midst of a recession. So the current period is unique. Interest rates, unemployment, and inflation are all low by historical standards. And this would be the first rate cut in over a decade. Plus there’s the fact that stocks have once again been hitting all-time highs in recent weeks. It’s quite possible the only reason the Fed began its hiking cycle in late-2015 is to give themselves the option to then cut rates yet again, which appears to be the current strategy. In the short-term, any Fed actions likely provide more of a psychological impact on the markets than a lasting change in fundamentals. The short-term impact on the markets will always be driven by whichever story investors decide to latch onto. Some will assume a rate cut will signal a weakening economy. Others will assume the Fed will ease in time to keep the party going. Eventually, those short-term narratives have to be backed up by long-term fundamentals or they run the risk of being outed as frauds. Even with nearly 140 rate cuts since 1960, there have been 30 double-digit stock market corrections and 8 recessions in the U.S. over that time. Regardless of what they do, the Fed can't fight off recessions or bear markets forever. |